Still Feel Behind in Retirement Savings? Why 2025 Is the Year to Take Action

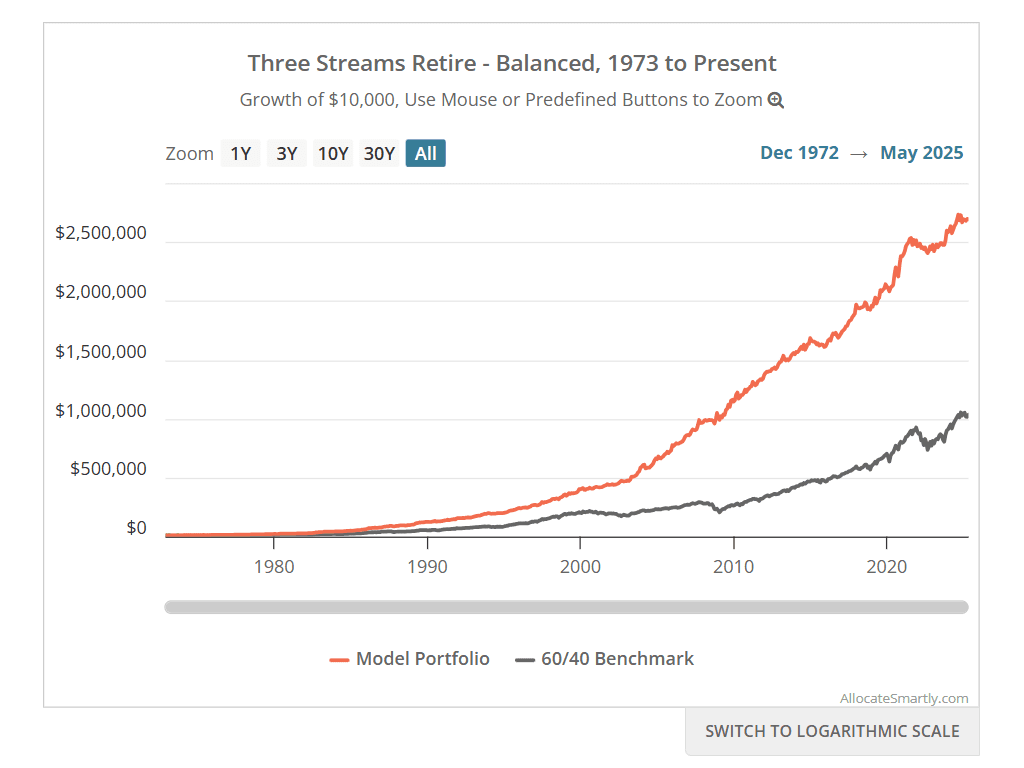

Chart Source: AllocateSmartly.com

Still Feel Behind in Retirement Savings? Why 2025 Is the Year to Take Action

Still feel behind in your retirement savings? You’re not alone—and you’re not out of time. A year ago, we introduced three innovative strategies to help late savers take control of their future (see: Feel Behind in Your Retirement Savings? 3 Steps To Take Now). With market conditions shifting and interest rates steady, 2025 may be your most critical window yet.

At Three Streams Financial, we’ve helped countless families and professionals use these exact strategies to build resilience, boost income, and confidently retire.

This post will discuss:

- Why managing drawdowns is rule #1 if you feel behind

- How dividend income offers smarter, inflation-adjusted cash flow

- New 2025 updates to catch-up contributions and withdrawal strategies

Are you behind—or just waiting to catch your stride?

What Is Feeling Behind in Retirement Savings—and Why It Matters

Many investors believe they’ve missed the boat. But the real risk isn’t being behind—it’s failing to act. Inaction can be more damaging than any late start, especially in today’s high-valuation, post-COVID market environment.

Why 2025 Presents a Unique Opportunity for Retirement Planning

1. Avoiding Drawdowns Is Rule #1

Markets remain near record highs—but risks persist. The Shiller CAPE ratio continues to flash warning signs, and global uncertainty hasn’t disappeared. For those nearing retirement, now is the time to protect what you’ve built.

Sequence-of-returns risk is real.

Losses early in retirement can cause irreversible damage. That’s why smart investors focus on limiting drawdowns rather than chasing returns.

Smart moves for 2025:

- Use buffer ETFs to stay invested while minimizing downside.

- Incorporate risk overlays like trend-following and volatility targeting.

- Build multiple income sources so you’re never forced to sell low.

Focusing on “losing less” beats picking winners when time is short.

2. Focus on Dividend Cash Flow—Not Just Growth

Dividend Growth Investing is more than a strategy—it’s a mindset. And in 2025, it’s essential.

Why it works:

- Sticky inflation demands rising income, not just fixed yields.

- Dividend Aristocrats have consistently raised payouts—even in volatile years.

- Qualified dividends provide tax-efficient cash flow for retirees.

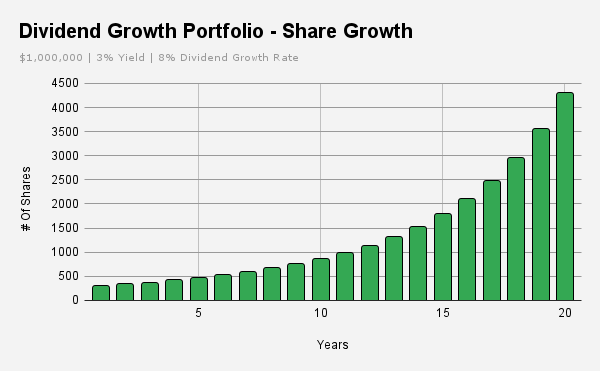

A $500,000 investment in a diversified dividend growth portfolio could double your annual income over 20 years, assuming 6–7% dividend growth and reinvestment.

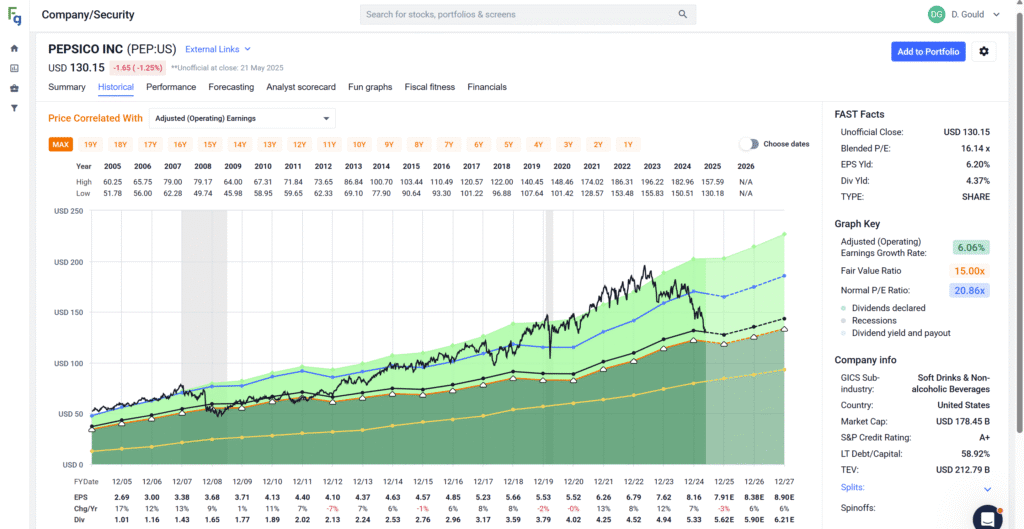

PepsiCo—recently added to client portfolios—continues to raise dividends despite market noise. That’s the kind of consistency retirement plans need.

Chart Source: FastGraphs.com

3. Catch-Up Contributions + Smarter Withdrawals

For savers age 50+, 2025 brings new tools for building back faster.

Key updates for 2025:

- 401(k) catch-up limits have been raised.

- Secure 2.0 legislation allows Roth catch-up options in employer plans.

- Delaying Social Security now pays more—8% annual increase + inflation adjustments.

Pair those changes with a flexible withdrawal strategy—cutting back during downturns and drawing more during bull runs—and you can significantly extend your portfolio’s lifespan.

What the Trends Say

Dividend Income Growth Over Time

This visual illustrates why 2025 is a critical year to take action: Delayed action shrinks compounding power. Starting now maximizes future income.

In Conclusion

You’re not behind—you’re just getting started.

The opportunity to catch up is real—but only if you act. At Three Streams Financial, we help clients minimize drawdowns, build tax-efficient income, and confidently retire—even if they’ve felt behind for years.

You don’t have to be perfect. You need a plan that works.

Three Streams Financial is an independent, fee-only investment advisor that confidently helps working families and professionals retire. Contact us if you’re looking for tailored insights and a clear dividend income strategy.

Key Takeaways

- Sequence-of-returns risk remains a top threat—mitigate it through diversification and drawdown control.

- Dividend growth investing offers rising, inflation-adjusted income.

- 2025 updates to catch-up limits and Social Security make this a pivotal year.

- Consult a fee-only fiduciary financial advisor before making investment decisions.

Fee-Only Advice. Proven Process. Transparent Planning.

Remember, there’s no one-size-fits-all approach to investing. Do research carefully, consider personal circumstances, and consult a fee-only financial advisor before making investment decisions.